Wealthy Rabbits with RRSPs

Special Guest Robert R. Brown

Robert R. Brown is a freelance personal finance writer and the author of Wealthing Like Rabbits – An Original Introduction to Personal Finance. He lives in Ajax, Ontario with his wife Belinda and their three kids Jennifer, Jessica and Christopher. Learn more about Rob by visiting www.wealthinglikerabbits.com

Resource List

Here is a list of the resources we used for this episode!

Transcript

Jackson: Jackson Middleton

Robb: Robb Engen

Sandi: Sandi Martin

Rob: Robert R. Brown

And go.

Jackson: Hey everybody, welcome to another episode of The Because Money Podcast. This is Episode 27, the most exciting episode we’ve had so far. And with that, I’ve got nothing else to say and I’m turning it over to Robb Engen. Robb?

Robb: Thanks Jackson and welcome everyone. We’re really excited to have Robert Brown here, author of “Wealthing Like Rabbits“. I believe I was quoted in this book now in the second edition as saying, “This is the most entertaining personal finance book since David Chilton brought the Wealthy Barber back out of retirement.” So thanks for including that, Rob, and welcome to the show.

Rob: Thanks for having me on the show, Robb, and thanks for reading my book. You know, anytime a personal finance author is compared to David Chilton, it’s a real honour, so thank you for that.

Robb: So we’re here talking about RRSPs. and you know RRSP season, it’s a magical time of year when the banks and their PR firms trot out those surveys talking about how Canadians are not prepared for retirement; we haven’t saved enough. And that magic cure is saving more inside your RRSP. Sandi Martin used to work for a bank and I love it when you call it this, it’s “RRSP hunting season”. Time to get ready because your banker’s coming for you and your money and your contribution, and I wondered maybe if you could tell us a little bit about your experience on the dark side with RRSP season, and what that meant to the banks and how you felt during that time.

Sandi: Well RRSP season starts on December 1st when you get a list of outbound calls to make. So these days with anti-spam and you know—what’s it called? It’s not teleconferencing, it’s that thing you do when you call people. Whatever, that stuff. [editor’s note: she’s thinking of telemarketing. Forgive her, she’s tired] You have to have a legitimate reason to call somebody – I mean, big data is at work at the banks. So if you have a product at the bank, your name shows up on a list. So, if it’s an RRSP-type product, then I can just call you and say—well, in my old life—I could just call you and say, “Mr. Client, it’s RRSP season. Have you thought about when you’re going to make your contribution? Why don’t you come in and see me. I’ve got some time next Friday at 2 o’clock.”

If someone has got like a VISA card, or not an RRSP, I have to make it more roundabout, obviously, because we have to come up with a legitimate reason to be calling them. But you get these lists on December 1st and they are massive. There’s like pages and pages. And keep in mind, at the end of my career, I worked in a very small town, a very small bank branch, and I had pages. And this is the time of year where you have to make 25 outbound—brand new, not returning calls or anything else—outbound calls a day and you need to be pre-booking at least 10 appointments for the next week. And if you’re not doing that, and if you’re not calling all the people, and if not everybody on the list gets called, then you are in trouble. And there are incentives; you can get things like a steam cleaner. There’s ridiculous things that happen.

So RRSP season is very much the time of year–except for home power line of credit season in the spring–it’s the time you where everybody knows what your job is in that back office. And that is to get people and their investment dollars in the bank.

Robb: Right. Rob, why don’t’ you tell us your thoughts. Obviously this is self-serving for the banks. They publish these surveys, “We’re not saving enough” they want to scare us. There’s certainly a call to action because there’s a deadline this year, it’s March 2nd. You’ve got to have your contribution in for 2014.

Like what is your take on the job the banks are doing. First of all, are we saving enough for retirement? So is reading about that a good thing, I guess, for the average Canadian to kind of spur them into action? Or is this just self-serving from the banks?

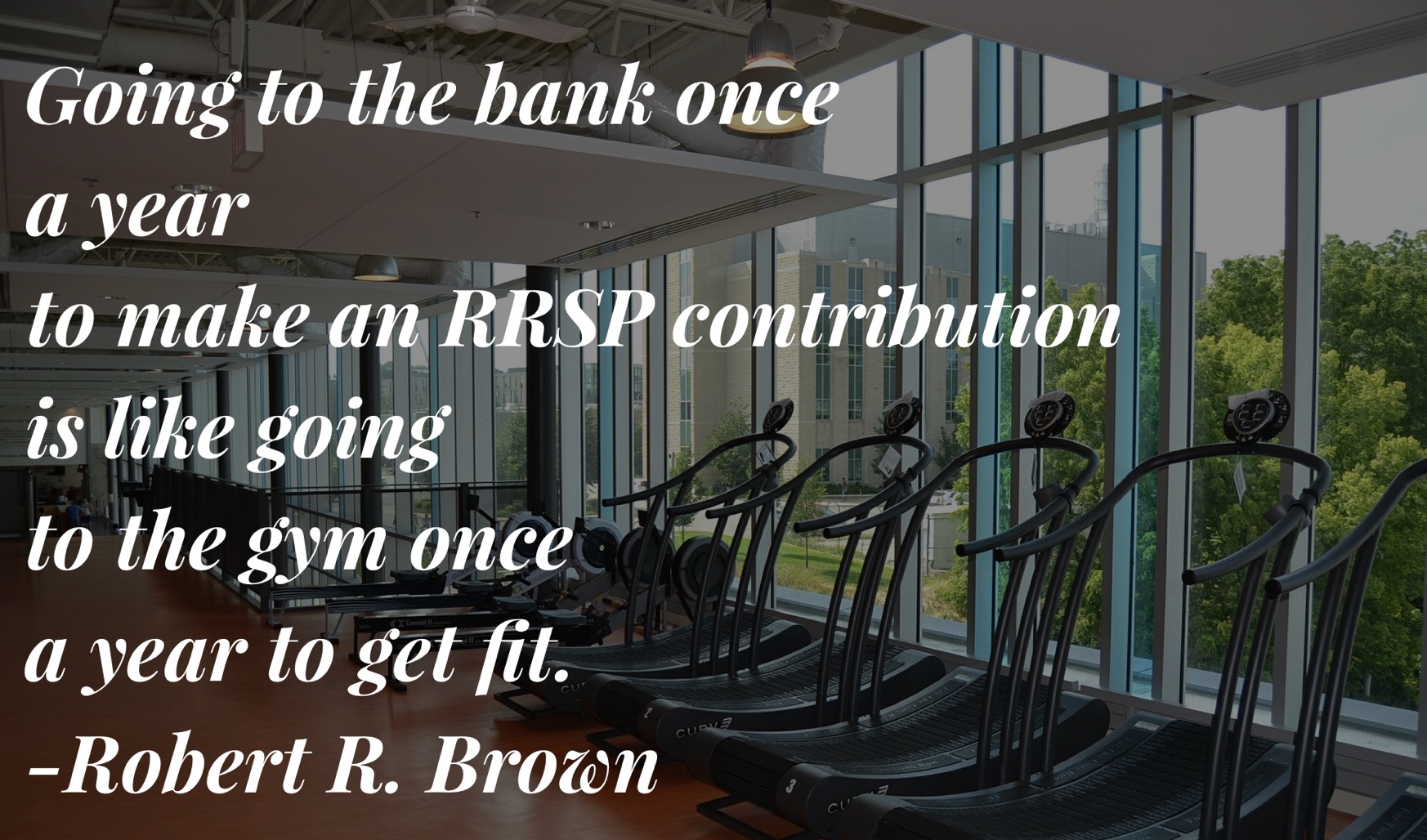

Rob: I think a bit of each. I think it’s fair to say that broadly speaking, Canadians are not saving enough for their retirement. But that said, just going to the bank every February and making a lump sum contribution to an RRSP and calling that a retirement plan is a lot like going to the gym once a year and calling that a health and fitness plan.

An RRSP can be a valuable product in terms of your overall financial plan, but just going to the bank every February and dumping a couple thousand dollars in without considering whether or not that it’s the right move, whether or not that’s the right product for you, is just not thought out enough.

Robb: Jackson, have you got phone call yet? That RRSP phone call from your bank?

Jackson: No, my bankers don’t phone me anymore. I’ve removed myself from all banking except for Tangerine, and that’s fun online. But no, I certainly don’t get the calls. Sorry, you caught me live tweeting that, and then I realized we don’t even do live tweeting on this show anymore.

But going to the bank once a year to make an RRSP contribution’s like going to gym once year and calling yourself fit. To me, that’s brilliant. I’m going to put that on the internet, and then it will be for everyone to see.

Robb: So what’s a better way then? Obviously, first of all there’s making your lump sum contribution in February, and I don’t know if this was from the days of old when we used to get year-end bonuses in January or February. I don’t know. I haven’t seen a bonus in quite a few years. But maybe that has happened and people would deposit their bonus.

But what I think is happening more and more is that we don’t have the money, so we need to make that contribution, we need to make it by March 2nd. And so what are the banks going to offer us? It’s a top-up loan or a catch-up loan. And what are some other traps that that come into play there?

Rob: Well, you know, in very broad terms I’m not necessarily a fan of the RRSP loan either. Obviously there’s exceptions to the rule. Some people can then take a refund, put it against that loan and then pay it off quickly and there are varying circumstances. But for most people, when they get an RRSP loan, they’re now in a position where they need to make payments, which may prevent them from paying themselves first in their RRSP for future years.

So they’re kind of behind that curve a little bit, and they’re paying interest to a bank while they’re behind it. So I’m more a fan of setting up a regular savings plan, a “pay yourself first” plan, whether it’s to an RRSP or a tax-free savings account. But like going to that gym two or three times a week for that overall part of your fitness program, doing it consistently throughout the year, as opposed to that one time a year when you feel like it’s a bit of a knee-jerk reaction. You might not be buying the right product for yourself, and then you don’t look at it again till the next year.

Sandi: And it’s panic too, right?

Rob: Sure:

Sandi: Like there are people that will come in on February 28th, or if you’re lucky maybe February 29th. I mean, you used to have to book time. You would know that it’s RRSP season and that it’s the last week of February and so I’m going to be getting home at 7:00 or 8:00 at night, even though the bank actually closes at 4:30 or 5:00.

And then there’s that feeling. On the one hand, of course, I kind of believe any Machiavellian thing about the bank that I can possibly believe. On the other hand, I think people create that panic for themselves. So I don’t know that it’s necessarily the bank saying “Well look, if we rush them we can sell them any product we want,” although I don’t think that they are against selling any product that they want, like “Oh, put it into monthly income fund. No big deal.” But I think people, this March 2nd deadline that people have, they get so scared about it and they’ll kind of do whatever’s suggested when they get to the bank, because they don’t want to go back two weeks later and actually talk about he reasons why they should be or should not be contributing to an RRSP at all.

Robb: And I find the deadline too is sometimes more about the refund than anything, right. I think we just have this fear of owing taxes in April. And so, okay well what do I need to do? I need to make a $5,000 RRSP contribution or $10,000, so I can get that refund, so that I can make my summer vacation plans or buy that big screen TV, or pay off the credit card. Isn’t that part of the trap too?

Sandi: Sorry, I just need to say one other thing. There are some people, a small group of people, who really do take conscious advantage out knowing exactly how much income they made between January 1st and December 31st and are taking that time afterwards to go through their taxes and come up with, based on that income, the optimal strategy for them to put this amount into RRSPs. They can do that because they know that information precisely since the previous year’s information is in and it’s not just back of the envelope. And some of those people might be self-employed people, so that structure can actually really help some people, but again, I don’t think that as many people take advantage of it as should.

Rob: Sure.

Jackson: I’m going to jump in and say, you know, back when I was a mortgage broker, I would get calls around RRSP season, talking about the Home Buyers’ Plan. You know, people wanting to make a contribution because of course to use the Home Buyers’ Plan, you have to have your money in for 90 days. So it’s like okay, I’ll do it if I get a rebate. So they were concerned about making a downpayment. Now, does everybody? No, but I did have calls.

You know, I think the arbitrary deadline, the scare tactic, fear-mongering deadline that’s there. You know, the banks of course used it to get people thinking, but hey, if it gets them saving money, is it necessarily a bad thing? But if they’re buying bad products, maybe. But as part of the Home Buyers’ Plan, it certainly worked out in my favour as a mortgage broker.

Robb: Rob, you had some thoughts on the Home Buyers’ Plan, don’t you?

Rob: Yeah, in broad terms I’m not a fan of the Home Buyers’ Plan. I think an RRSP is designed to save for your—to be honest, I’m not a fan of the phrase “retirement.” I prefer “long-term saving,”—to set some money aside for your future. The Home Buyers’ Plan allows you to dip into that to save some money or take some money out for the downpayment on a home, but I don’t think a lot of people think about the long-term repercussions on what they’re doing to their retirement, or their long-term savings over the long-term.

I would prefer, and again, it’s personal finance so every situation’s a little bit different. I would prefer that people actually just reduce the amount they’re putting in their RRSP while they’re saving for a downpayment, then use their tax-free savings account to save for that downpayment so they don’t hurt their overall long-term savings plan as much as possible.

Jackson: I guess from my experience as a mortgage broker, I’ve never really found many responsible young people, and I think the Home Buyers’ Plan has served its purpose. I’m certainly not going to take a stance here, but most people would say, “I’m going to borrow against my RRSP so that I’ve got the appreciating value on my house.” Because a lot of Canadians would look at their house as their long-term savings.

Whether you disagree or agree with it, I think that’s kind of the perception that a lot of people have is the RRSPs on one side, home ownership on the other is the same thing because they’re both appreciating. As we enter a situation in Canada where house prices might drop, it might start to freak everybody out, but for the last however many years, all we’ve seen is appreciation.

Robb: House prices will never drop, Jackson.

Jackson: Ever, ever, ever.

[laughs]

Rob: And Jackson, I agree with you, that a lot of people may use their RRSP to buy their house because they see their house as their long-term savings. But a little bell always goes off in my head whenever somebody mixes up that the two components of that personal finance plan: their house and their long-term savings.

So whenever somebody says that their house is their retirement savings plan, a bell goes off in my head because they’re going to need to sell that asset at some point. They’re going to need to live somewhere, and people typically don’t make as much money on their home after the cost of selling that comes out.

Alternately, whenever somebody goes into their retirement savings plan to buy a home, they’ve hurt that other component, that savings plan, so that they can’t move forward. They have to look at both. I’m sorry, you can’t just rob Peter to pay Paul. A long-term financial plan needs to include both.

Jackson: I agree with you on that.

Robb: Just sticking on the RRSP train here, and now with the introduction of tax-free savings accounts, that gives people an option that a lot of us didn’t have when it came to saving while using something like the Home Buyers’ Plan. I started saving inside an RRSP when I was 19, I think. So there was none of these calculations about I’m only make $20K a year. The math is not going to work out on the other side. I just thought that was a vehicle to save for my long-term retirement.

But unfortunately, I ended up having to raid that’s plan and pay off some debts, and then start all over again. So I wish there were something like a tax-free savings account back then. However, there is now, and so that kind of leads me into we’ve got this, again, RRSP season. Make your annual contribution or borrow to do it, but as Sandi alluded to earlier, we’re maybe not talking enough about who should be contributing and if an RRSP is better for you, or should we just be saving inside a tax-free savings account.

So since that’s been introduced now, what are some of the choices now? Who should be saving inside an RRSP and who should be maybe leaning towards a tax-free savings account?

Rob: Well first of all, Robb, congratulations to you for starting an RRSP when you were 19. When I was 19, I was still trying to figure out how to peel the label off a stubby without ripping it, so good for you.

And when we talk about the RRSP versus tax-free savings kind of debate, I think it’s important to start here. Making the decision to be committed to a long-term or a retirement savings plan, and following through on that commitment is far more important than which of the two products you choose.

I’ve had this conversation with people who haven’t even started to save yet, or only have a couple thousand dollars in the bank. Yet they’re more concerned with which product they should be choosing rather than having that long-term savings plan started. It’s kind of like to use that overused gym analogy again, it’s like when you go to the gym should you be doing your cardio on the elliptical or the treadmill? They’re both great products and they both have pros and cons, but the fact that you’re going to the gym and doing the workout is important, just like that you’re saving and the two products are both savings. They’re both very good products.

Robb: Absolutely, and I think what a lot of people don’t realize, if they only look at something called the tax-free savings account and “Oh, I can withdraw money tax-free.” And we’re still kind of got our heads wrapped around the tax concerns around that. And so they think tax-free savings account. That’s what I want because I don’t want to have to pay taxes on my withdrawals. But an RRSP and a tax-free savings account are just mirror images. So the idea behind it is I put in a thousand dollar contribution into my tax-free savings account, well I’m using after-tax dollars to do that. And when I withdraw it, it’s tax-free. But when I put in a thousand dollars into my RRSP and then I get that $400 refund. And then I reinvest that refund—that’s the key. And when I withdraw it at the end, it actually works out to be the same.

I guess we don’t know. What is going to win out in the end is your tax bracket when you take out the money. So unfortunately, we don’t know that in advance and so how do we decide? Maybe I’ll kick it over to Sandi and ask who would be better off making an RRSP contribution now verses a TFSA, or should you be doing both?

Sandi: So what’s your taxable income going to be in retirement? if you have enough money saved, probably it’s going to be more than $24K for a couple, right? That’s if they get the maximum amount of CPP each. So obviously, then if you’re making more than $24K, maybe you should put it into an RRSP instead of a TFSA, but that’s just the start of the calculation.

Sorry, that is a really difficult question to answer, Robb, because most of us don’t sit down and chart out our lifetime taxes. That just seems like it an obnoxious task to do. [laughs] Not only does it sound obnoxious, it’s almost impossible. You have to make series of assumptions about your earnings potential and what the tax brackets are going to be like later.

But if you were to do so, and if you were kind of to make a series of assumptions and then kind of work consistently with those assumptions. So I’m going to assume that I’m always going to make more than $45,000 every single year, well then theoretically it make sense if you’re going to be then earning less, or if you have less that $45K of income in retirement, then you ought to be putting money into an RRSP while you earn that $45K. And when you take it out at $30K or $26K, then ideally you’ve kind of played that tax game, right? You’ve paid less tax than you would have if you’d just spent that extra money that you were saving when you were earning $45K.

Robb: We had a show a while back that talked about optimizing your finances, and just like you’ve said there, who sits down and actually figures out their lifetime taxes paid? And like what Rob said about just the act of saving is that we’re winning there, so at the end of the day does it matter? Unless there’s a huge gap in your taxes between now and retirement, or where you’re going to live maybe, does it really matter?

Sandi: It can matter an awful lot for people who have very limited income. But if you’re really responsible with a really low income now, and you’re really responsible in what little you can save, you save it in an RRSP because that’s what you’re told and that’s when the deadline is, and that’s what the banks all talk about, and that’s what they called you for. Then in retirement, some of the things that you should be able to access, like Guaranteed Income Supplement, some of the programs like the tax credits for people that are means-tested, you won’t get them because you unfortunately saved your money in an RRSP, and when that money when it comes out it was taxable instead of tax free like it would be from the TFSA.

That doesn’t mean that it’s a scam. It doesn’t mean that, “And then the government got me and they charged me in taxes” and whatever, it just means that not a lot of people trumpet the benefits of the tax-free savings account for people with lower incomes, as a vehicle for what Robert is saying, for long-term savings. It’s just marketed as the tax-free savings account for your emergency fund for next year.

Robb: Rob, what’s your take on that RRSPs are just a government scam. “I put in this money and now I’m ready to retire. I had a million dollars in there and now they’re taking forty cents to every dollar. This is ridiculous.”?

Rob: Actually I touch on that in my book, “Wealthing Like Rabbits“, and I forget my exact wording, but I sincerely hope when I turned 71 that I have enough money in my RRSP that I get clawed back the maximum that can be clawed back and get taxed at the highest possible tax bracket. Because in order for that to happen, I have to have a substantial amount of money coming out of my RRSP through a RRIF every year. It’s not a bad problem to have.

Now, like everybody else, I want to manage my tax burden responsibly and do everything legal to reduce it, but having to pay taxes at 71 is not the worst problem in the world. And to allude to what you said Robb, you have to understand, you haven’t paid tax on that money yet. It went in when you were 25, 35, or 45 tax-free, and that’s the way RRSPs work.

To Sandi’s point, I absolutely agree for low-income earners, and for low-income earners as they approach their prime that the math might make more sense on the tax-free savings account. But there’s some caveats with that. Sandi said “disciplined and responsible.” If someone at 26 is going to start their long-term savings in a tax-free savings account, they can overall do better, but it’s important they leave it in the tax-free savings account.

One of the points I make inside the book is that tax-free savings accounts are often raided to buy a house or to buy a car to go on vacation, or to pay off debt; all of which are good things, but that doesn’t contribute to your retirement savings. That’s why I kind of lean toward RRSPs because if you take it out too early, you’re going to get taxed very heavily at first. And hopefully that will act as a deterrent. Now just lots of people take money outside of their RRSPs and pay the tax anyhow, so that argument can be played the other way.

Robb: Yeah, and that leads me another strategy, because a lot of people are now complaining about the mandatory withdrawal rates from your RRIF, and short of introducing new policy or legislation around that, Rob, what are some strategies that someone in their mid to late-50s or early 60s can do to help mitigate some of that. If that’s something that they’re concerned about is paying hefty taxes on their withdrawals. I kind of had an idea around this, but it’s so far away for me—no offense to anyone out there who’s in that situation. [laughs]

Thirty years from now I’d like to think that hopefully I’ve withdrawn my RRSP, or I’m in the process of it before I turn 71, and that I’m living off of that income in my financial independence, hopefully. And I’m also still saving inside my tax-free savings account, so that when I’ve depleted that RRSP, I’ve now got this hopefully something like a million dollar tax-free savings account portfolio that can now become my nest egg that I’m making tax-free withdrawals from.

I know with the tax-free savings account was introduced in 2009, and that with $5K and now $5,500 in contribution room. Probably too little for someone who was ready to retire, to take full advantage and do something like this. But is that a legitimate strategy do you think for people trying maximize their buckets of income in retirement?

Rob: Sure it is. Depending upon personal situation and your incomes in your 60s, you can start to pull that money out of your RRSP a little bit early, if it doesn’t create a tax burden at that time, and start to reduce the amount of tax you pay when it comes out as a RRIF.

I had another point to make, but I forget what it was. [laughs]

Sandi: You have my problem. [laughs]

Rob: I do.

Sandi: So here’s the thing though. I think what we’re talking about, with RRSP season and what you were saying about taking your RRIF before age 72: there’s defaults in place for all of these products. We all have defaults and the end result is what you said, Rob. If we follow the defaults, if we just kind of go in and make a lump sum contribution before March 2nd, and we’re maxing out our RRSP because that’s what they say to do, and we wait and we take it out at age 72, probably we’re going to be okay. Like if we’re at the point where we’re saving, but we’re just not saving optimally, we’re going to be okay.

But of course, also once you get to where you graduate from “I’m just going to do whatever defaults are” and you move on towards “I’m going to do this in a way that makes a little bit more sense for my own personal situation,” then you realize the defaults have nothing to do with you. I mean, obviously there’s a maximum amount that you can contribute, but aside from that you don’t have to wait until 72. You don’t have to take your CPP at 65. You don’t have to contribute on March 1st to your RRSP. But you can, and if you do, you’ll probably be fine, even if it’s not optimal for you.

Rob: Agreed.

Robb: And I think that’s why there may be a lot of angst around that retirement age, and when can I retire. It’s because there are so many variables outside of the default, right Sandi? If you have a defined benefit pension and you’re reaching the age where your normal retirement age, and then maybe you have some savings outside of there. And that’s when you start to do some major calculations and could probably use the help of an advisor or someone that you can trust to help you through those calculations.

I think you’ve had posts on this before, Sandi, I think you called it “Necessity Tetris.” All those buckets of income. So you talked about CPP and your RRSP or you’ve converted it to a RRIF, your tax-free savings accounts, and all those things. There’s so many different pieces to it that it becomes really hard. Is it almost too complicated to assemble that?

Sandi: I can’t say that it’s too complicated, because if it was something really simple and easy, and universal for everyone, in some ways—this is obviously just kind of my own default position—in some ways it must be inequitable. If it’s easy for everyone, there’s got to be some big glaring hole it’s not addressing. So when it’s little pieces kind of overlapping, it means that the government or policymakers have the ability to address small injustices or inequities without revamping the whole program.

So in a way I can see why it doesn’t seem so, but it is sort of an efficient way to address saving for your own personal retirement. I don’t think it’s too hard—and actually this is a point that I remember Rob making in his book—people should not be so intimidated by this information that their default is, “Oh, I better go talk to a professional about it,” even though that’s how I make my living, it’s not rocket science. All of the rules for each puzzle piece that you have to put together, or each Tetris piece that falls, each rule is very clearly defined. You can call Revenue Canada about RRSPs. You can find out it. You can call Service Canada about your CPP. You can outline all the rules, and if you think about it long enough or have a good framework and are able to do research and read, you can come up with a good strategy for yourself.

I think the reason people maybe ought to talk to somebody, sometimes, is just to have that sober second-thought and to make sure they’re not missing anything. If this is something that they’re doing once for themselves and have never done it before, and probably won’t do it again. But that doesn’t mean that you have to immediately get panicked and say, “I better go talk to a financial professional because I don’t know what I’m doing.”

Robb: One last thing I wanted to throw back at Rob was we’re kind of may be circling back here to the point about the RRSP deadline. Sure there’s going to be a lot of appointments. You’ve got a phone call from your advisor, you’ve come in to see him or her, and what are some of the things maybe you should be wary about in that meeting? You’ve got kind of that looming deadline. Are you just worried about making a contribution, but what about where is your money going to go? Is it going to go into the GIC, is it going to go into an equity mutual fund that has a 2.5% MER? What are some of the pitfalls you should avoid when you’re under the gun? Or what are some of the questions you should ask your advisor when you do go in for that RRSP season meeting?

Rob: Well, that’s a tough question. I guess I would go to that meeting not necessarily feeling I had to do anything. Just to first of all gain information. I tend not to do anything when I feel like I’m under the gun, because that’s when kneejerk and bad decisions are made. If you’re in a position where you can afford to make a lump sum contribution to your RRSP and you’re facing a deadline, not a great position to be in, but not the end of the world—as Sandi said—either.

I would probably just at that point put it into cash or into short-term GIC, only until you’ve had a chance to sit back and think about what the best investment decision is for you, as opposed to making one quickly that you could regret.

Robb: I remember once when I was younger and I was up against a deadline and facing a $2,000 tax burden and I was talked into making a $7K contribution, and it went into some index-linked GIC that, of course, I’ve learned all about later on in my life, that they’re maybe not the best products, or that was maybe not the best choice.

Jackson: Not the worst choice.

Rob: Yeah, not the worst choice. But I certainly did feel that pressure that I needed to make that contribution and this is what was put in front of me, so I did it. So I like the idea of going into it, hopefully your meeting isn’t on March 2nd, because that would make it tough to take it home and sleep on it. But going into that meeting as a fact-finding mission rather than an “I need to do something right now.”

Sandi: Sorry, you can always park it in cash. You can put it into an RRSP cash account on March 2nd at midnight if you want to. Well, not midnight, at 11:59 let’s say.

Robb: Sure. No, I like that. I guess my point is, if you’ve left your savings to a one-day kind of winner-take-all meeting with your advisor to make your contribution, that’s not necessarily the worst thing in the world. I guess my point is, try not to let any deadline, whether it’s a contribution deadline or you think you’re going to be faced with a tax liability deadline, try not to let that influence your behaviour or let someone, like your bank advisor, influence where or how much you end up contributing.

Rob: And I guess the other thing that I would add to that, if you have that feeling when March 3rd comes along, start to do some planning for next year so you don’t get into that same cycle again next year. If you had to this year, that’s unfortunate, but learn from it and take the steps necessary to make sure you’re not in same boat next year, because it’s coming.

Sandi: If RRSP season is really the way that it used to be when I was banking then the person you’re sitting across the desk from has just as much pressure and hardly any time to talk to you either. So really, how much real planning is getting done? Even with the best will in the world, how much real planning can you get done in the space of at most an hour-long appointment? You just can’t do it.

Rob: Sure.

Robb: Excellent, well I think that’s our time, but Rob, thank you so much for coming on the show.

Rob: Guys, thanks for having me. It’s was a lot of fun.

Robb: I know we didn’t get any zombie references in there, but maybe we can work that in with “It’s a zombie apocalypse” and “RRSP deadline is coming up, so…”

Rob: It’s been a long half an hour to go without a Star Trek reference, but I held it back.

[laughs]

Robb: Well that’s great. I hope to have you on again soon and thanks very much.

Rob: Thanks very much for having me, guys. It was a lot of fun.

Jackson: Good-bye.